Justifying Investment in Manufacturing Execution Systems

Executives at manufacturing companies of all sizes need to make decisions about where to invest to maintain and grow their businesses. Investments in manufacturing execution system (MES) applications may reduce costs and increase revenues, but they also might compete with other investment priorities, such as marketing campaigns and capital equipment upgrades. This article offers guidance for life sciences companies considering investment in manufacturing execution system applications, including how to measure MES-related cash flow and reasonably evaluate an investment in manufacturing execution system versus other alternatives.

Manufacturers considering investment in an manufacturing execution system may wish to consult the GAMP® Good Practice Guide: Manufacturing Execution Systems, 1 which provides an overview of issues to evaluate in a strategic assessment of MES options:

- The current status of the business pertaining to manufacturing system requirements

- The desired state of system requirements to be achieved, including a breakdown of high-level functionality required to advance the business while managing costs

- Analysis of desired functionality already in existing systems, and any needs for new systems to be added to the domain (automation, MES application, enterprise resource planning, quality control, data historian, etc.)

Operational Justification

Output from the strategic assessment provides a roadmap and justification for MES application functionality. Sometimes, the need for MES applications is so overwhelming that this evaluation simply provides the scope of implementation. If it is not possible to operate a process without MES functions, the entire business case for manufacturing the product is based on having MES applications in place.

For existing production facilities, the operational justification for the MES is typically based on quality and patient safety needs, such as nonconformances, corrective and preventive actions (CAPAs), customer complaints, and inspection/audit observations, as well as business needs, such as expansion plans, anticipated process/product changes, and overall business agility to meet as-yet-unknown demands.

For new operations, using an approach such as failure modes and effects analysis (FMEA) can identify risks that can be mitigated by implementing MES applications, such as the following:

- Data collection risks: The data collection rate or volume is too high for reliable manual recording.

- Raw material risks: The number of materials, the use of similar materials, or criticality of material additions introduces the chance that incorrect materials could be added or materials could be added in the wrong order.

- Sample tracking risks: The number of samples or complexity of sample management introduces high potential for sample misplacement or mislabeling.

- Manual operations risks: The complexity of manual operations increases the likelihood of operator error.

- Compliance risks: Other required documentation cannot be accurately and consistently completed by a human without additional human review or observation due to the complexity or quantity of the documentation.

Financial Justification

Even when an MES can be justified solely on the basis of quality, identifying additional financial justifications strengthens the business case and can garner additional support from the investment decision-makers. To financially justify a project, one must show that the company will profit by making this investment for current products or the investment will be necessary for future development.

A common metric used to evaluate or compare alternatives is return on investment (ROI). If there is only one alternative being considered, the evaluation is versus the current state, often referred to as the “base case.” The base case is what would happen if the investment were not made. Two common methods of calculating ROI are internal rate of return (IRR) and net present value (NPV). These calculations are very similar, so we will focus on NPV.

In addition to IRR or NPV, investments are sometimes evaluated based on a payback period (how long it takes for the investment to pay for itself). Using a payback period can sometimes be misleading because it only looks at how long it takes to “break even.” Two options may have the same payback period, but one alternative may continue to provide benefits for a much longer time than the other. It is also possible that one solution would require much greater future investment (maintenance). Both of these are differentiating factors that are reflected in the NPV.2

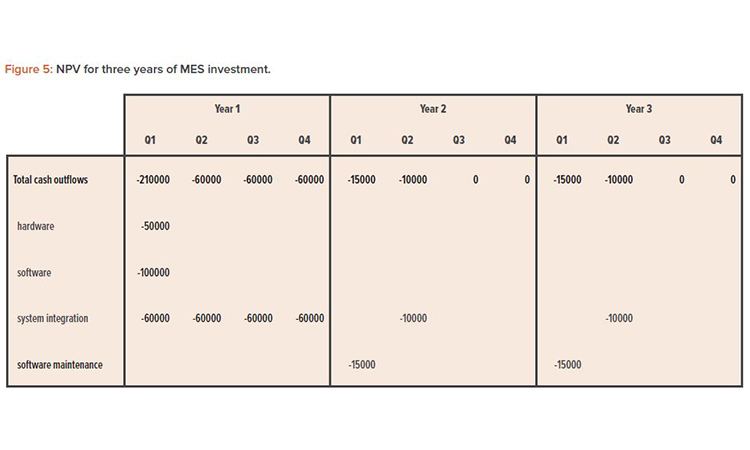

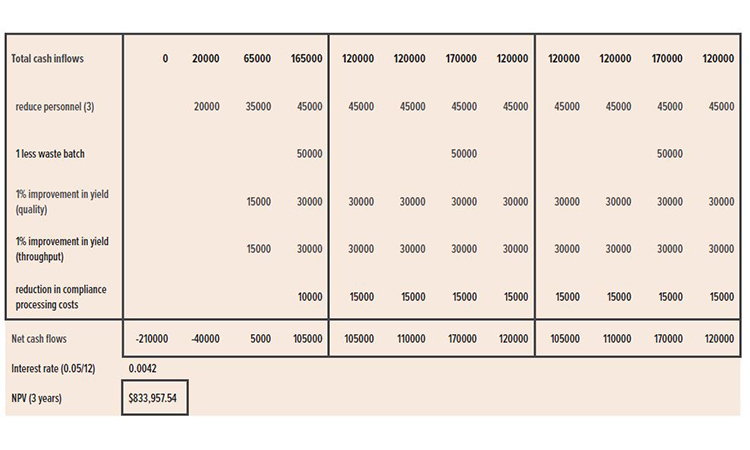

NPV Comparisons

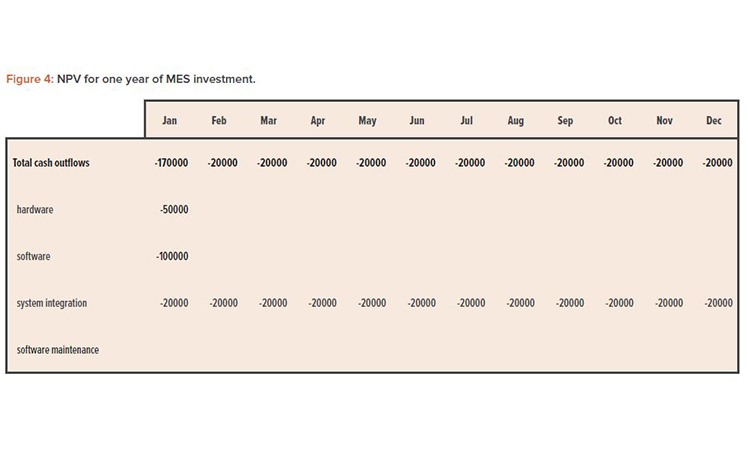

To calculate NPV, look at all incremental costs and incremental benefits over the life of the system.2 These are defined as cash flows—costs that must be spent to define, build, deploy, and maintain the MES (outflows), and real quantifiable benefits derived by having and using the MES (inflows). These are incremental because it is the difference between the proposed option and the base case, or between alternatives, that is important. For example, assume that the current system needs a server upgrade to continue functioning. In this situation, buying a new server for the MES is not an incremental cost because the new server is required regardless.

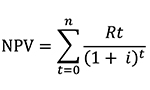

These costs and benefits (incremental cash inflows and outflows) occur over time. For example, the major cost of the MES occurs up front, whereas the cost savings occur over the following months and years. To make a fair comparison, costs or benefits that occur in later months or years are “discounted” to the present using a standard interest rate (often referred to as the “risk-free rate”). As an example, a quality improvement project that results in a rework cost reduction two years from now is not as valuable as having that reduction right now. The future reduction is discounted (to the present) so that it can be compared with all other costs and benefits, all discounted to the present (the NPV). This can be represented as:

In this equation, Rt is the sum of all incremental cash flows (in or out) in a period, t is time (typically measured in months, but can be years or days), and i is the discount rate (the return that could be had in a risk-free investment, such as a certificate of deposit) for that period. The discount rate is often set by the company finance department.

The NPV calculation is available in Microsoft Excel as “=NPV (rate, list of values).”

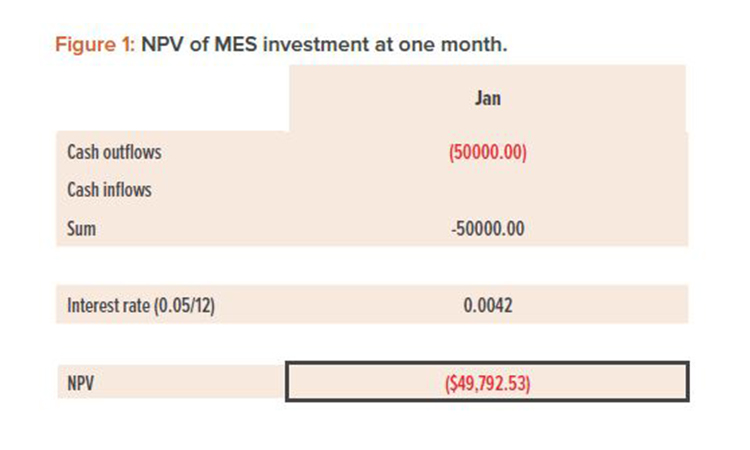

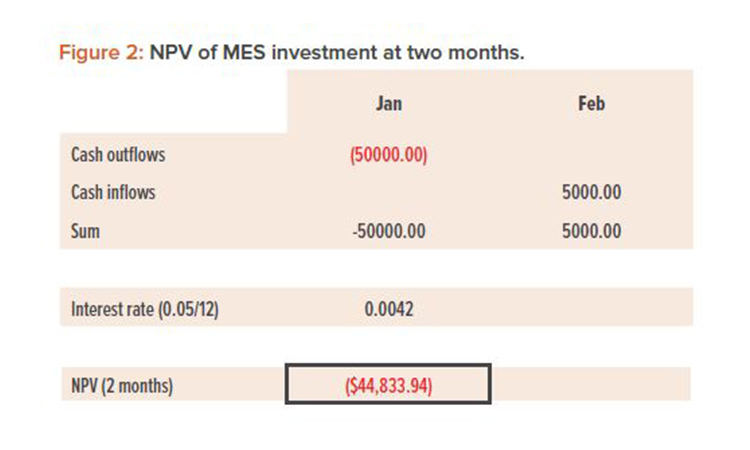

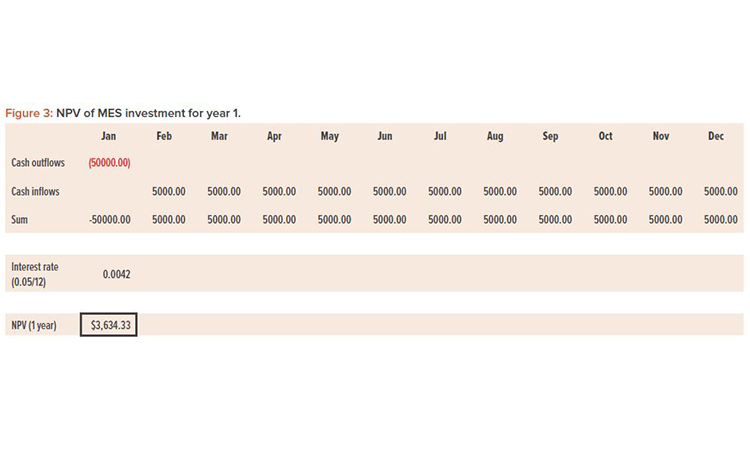

As a simple example, let’s say that in December (now), you are trying to decide whether to invest $50,000 in new MES applications. The entire investment can be made in January. Then, each month after that, the system reduces scrap by $5,000. We will look at one year. The finance department says they could invest that money at a risk-free annual rate of return of 5%. No other incremental cash flows have been identified.

The cash outflow in January will be $50,000. But that has to be discounted by the risk-free rate (0.42% per month). The NPV calculation using just the January cost is negative, as would be expected (Figure 1). On this basis, you would not do this project (negative NPV). Note that the $50,000 spent in January is equivalent to $49,790 spent now (that is, if you invested the $49,790 now at an annual rate of return of 5%, compounded monthly, you would have $50,000 in January).

To calculate net present value (NPV), look at all incremental costs and incremental benefits over the life of the system.

About the Author